We've integrated Spectral into Bulla's lending solutions!

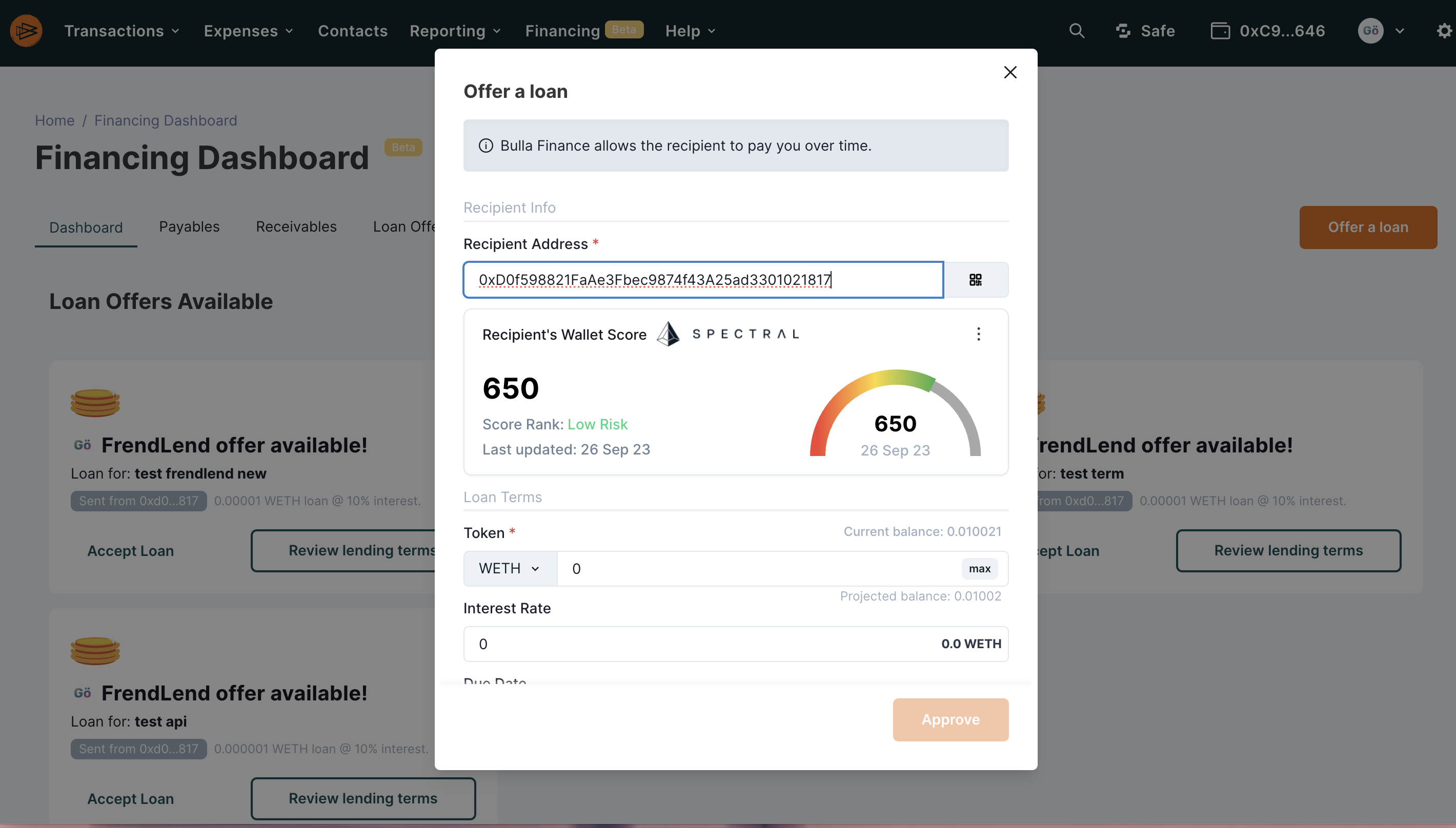

Bulla Network, a leading on-chain credit claim protocol and dApp, has integrated Spectral, an innovative web3 credit-scoring tool, into its lending solutions. The integration improves the on-chain lending process for both lenders and borrowers and helps promote on-chain capital efficiency. Bulla users that want to offer a p2p loan will now have the option of seeing their own web3 credit score as well as viewing the credit score of a potential borrower before setting loan terms.

Spectral generates the score by culling and compiling a comprehensive range of the user’s on-chain transaction data. The score shows up as a dashboard and rating in Bulla’s app.

“This tool is very exciting – it provides the highest level of transparency possible for our users, giving them more control over their lending and borrowing and ultimately more financial sovereignty,” said Mike Revy, Founder and CEO of Bulla Network.

“Spectral is a very exciting partner because the company is making ground-breaking inroads in the area of credit-scoring and we are looking forward to more innovations in the near future,” said Revy.

Traditional credit-scoring models use data from credit bureaus to generate a credit score. The exact data and algorithm used to calculate these scores, however, are not revealed to the consumer. There is a chance that a piece of data was not completely correct, a payment was mis-entered, for example, and the consumer may never understand why their score is low.

By contrast, Spectral uses publicly available blockchain data to provide users with a multi-asset credit risk oracle (MACRO) Score, which ranges from 300 to 850 and takes into account the widest possible range of on-chain transactions and data, including:

– All transactions, borrowings, repayments, deposits, redemptions, liquidations, etc, ever recorded on the lending protocols Compound and Aave.- Length of credit history, number of repayments, quantity of debt, and other debt-related metrics related to those borrowings.

- Wallet details such as the presence of high-volatility tokens, balance, average balance.

–Ethereum transactional data, e.g. token ERC-20 transfers.

–Various other public APIs for historical token prices in ETH which are used to derive consistent analysis.

- Market conditions

The process for then analyzing this data and generating a score is detailed on the Spectral website here: https://blog.spectral.finance/a-deeper-look-at-the-macro-score-part-one/ This method is transparent and indisputable because the data gathered exists on a public blockchain.

“There’s an enormous amount of blockchain data available,” says Spectral CEO Sishir Varghese. “We took four years of DeFi data, including hundreds of thousands of borrowing events to create the MACRO Score. The results speak for themselves.”

A recent capital efficiency simulation proved that MACRO Scores are capable of accurately identifying high and low risk borrowers, and boosting a protocol’s profitability, and is available here: https://blog.spectral.finance/proving-capital-efficiency-part-1/

And while this credit scoring method is still new, Spectral is already launching a new native web3 version of its methodology, one that will decentralize credit scoring completely and boost accuracy by allowing data scientists to compete for bounties and streaming payments. For details, please see: https://blog.spectral.finance/spectrals-vision-for-trustless-ml/

Spectral is a trustless machine learning oracle, best known for its on-chain creditworthiness assessment score. This year the company is releasing a platform that will allow data science challenges like credit scoring to be completely decentralized.